Solana and Base have emerged as two of the largest decentralized finance (DeFi) ecosystems, each managing more than $4 billion in Total Value Locked (TVL). While the two networks appear similar in size, their underlying strengths and market positioning differ considerably.

The Solana blockchain leads in network activity, processing significantly more active addresses, transactions, decentralized exchange (DEX) volume, and perpetual trading volume than Base. Its high throughput and low transaction costs have made it a preferred destination for trading, liquid staking, and speculative on-chain activity.

Base, Coinbase’s Ethereum Layer 2 network, has developed a different competitive advantage. Rather than maximizing transaction throughput, it has built a mature ecosystem around lending, Ethereum-native liquidity, and consumer-facing applications. Its protocol diversity and close integration with Ethereum position it as a strong platform for longer-term capital deployment.

This report compares the two ecosystems across four key areas:

- Capital position

- Network activity

- DeFi ecosystem

- Market positioning

The analysis highlights how the two ecosystems have evolved along different paths, with each leveraging distinct architectural and ecosystem advantages. Instead of viewing Solana and Base as direct competitors, the evidence suggests they occupy complementary roles within the multi-chain ecosystem.

Key Metrics at a Glance

Key Observations

- Solana leads in transaction activity, liquidity, and trading volume.

- Base has a more diverse protocol ecosystem and deeper lending infrastructure.

- Solana’s stablecoin supply is more than three times that of Base, supporting higher on-chain liquidity.

- Base benefits from Ethereum compatibility and Coinbase’s distribution, strengthening its position in consumer-facing DeFi.

Data Source

Unless otherwise stated, all quantitative data presented in this report were obtained from DefiLlama and represent a snapshot of on-chain activity as of July 9, 2026. All metrics represent conditions at the time of data collection and may change as on-chain activity evolves.

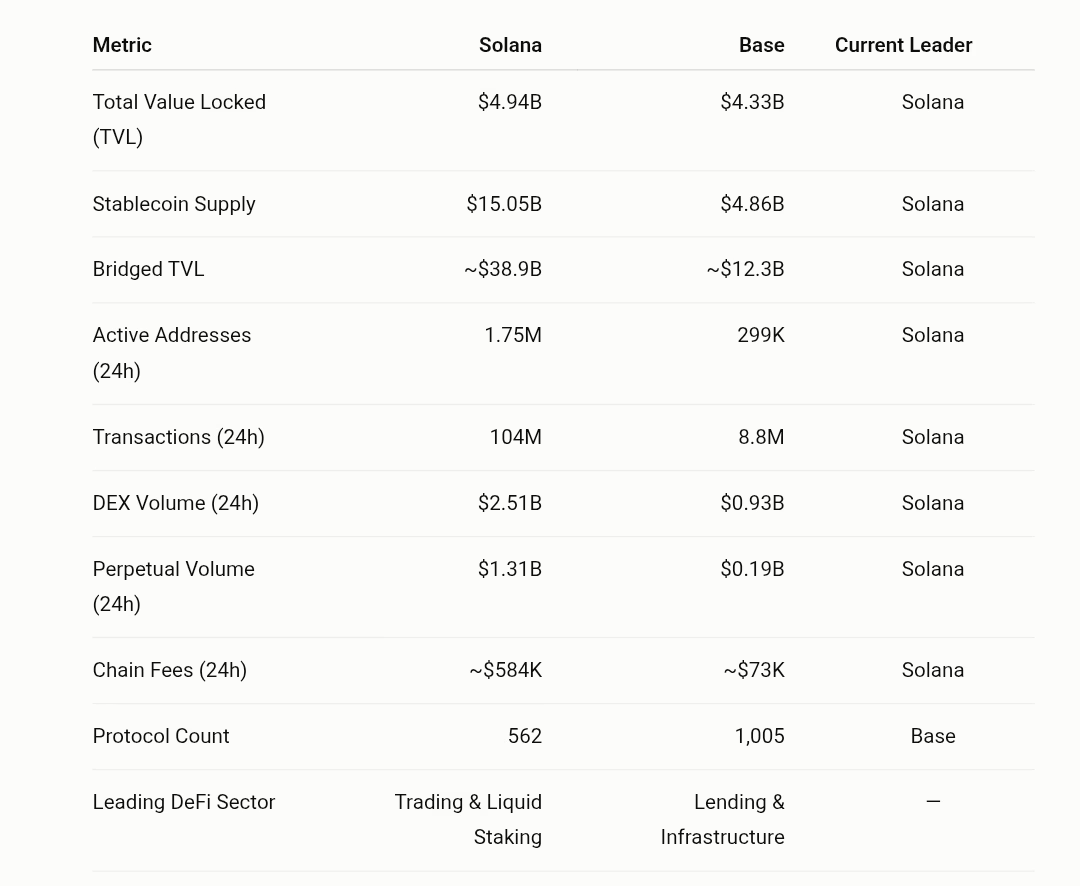

TVL & Capital Position

Total Value Locked remains one of the most widely used indicators for assessing the size of a DeFi ecosystem. It measures the value of digital assets deposited across decentralized applications, providing a snapshot of how much capital is actively deployed on a blockchain. While TVL does not measure network activity or user adoption, it offers an important starting point for comparing the relative scale of competing ecosystems.

As of July 9, 2026, Solana held approximately $4.94 billion in TVL, maintaining a modest lead over Base, which recorded $4.33 billion. Although the difference is relatively small, it shows that both networks have reached a similar level of capital formation despite following different growth trajectories.

But does similar TVL mean the two ecosystems are equally liquid? Not quite. A clearer picture emerges when stablecoin liquidity is taken into account.

Solana supports approximately $15.05 billion in circulating stablecoins, more than three times Base’s $4.86 billion. This larger liquidity base provides deeper trading markets and supports the high transaction volumes observed across Solana’s decentralized exchanges.

Where does that liquidity come from? Bridged assets provide another piece of the puzzle. Solana has accumulated approximately $38.9 billion in bridged assets, substantially exceeding Base’s $12.3 billion. This indicates that Solana attracts liquidity from a broader range of blockchain ecosystems, while Base primarily benefits from capital moving within Ethereum’s Layer 2 environment.

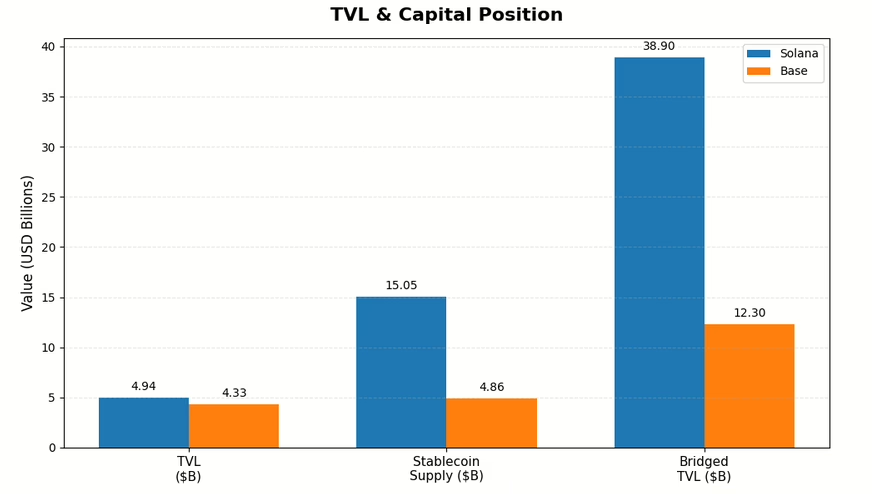

Network Activity

Capital alone does not tell the full story. How that capital moves across a network provides a better indication of user engagement and economic activity. Metrics such as active addresses, transaction count, trading volume, and fee generation help illustrate how heavily a blockchain is being used.

Across every major activity metric, Solana maintains a clear lead over Base. Over the 24 hours ending July 8, 2026, Solana recorded approximately 1.75 million active addresses, compared with 299,000 on Base. Although active addresses should not be interpreted as unique users, since individuals and applications can control multiple wallets, the difference points to significantly higher daily participation on Solana.

The gap becomes even more pronounced when looking at transaction throughput. Solana processed roughly 104 million transactions during the same period, while Base recorded approximately 8.8 million. This level of activity is made possible by Solana’s architecture, which combines fast block production with low transaction costs, allowing applications to process large volumes of on-chain activity efficiently.

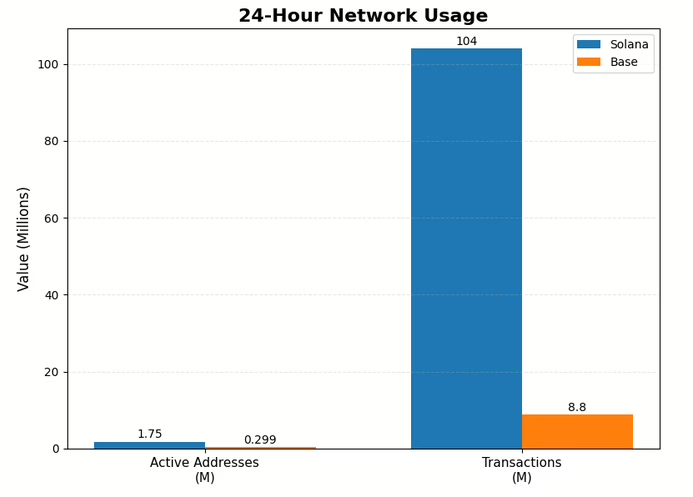

That same pattern extends to trading. Over the previous 24 hours, Solana generated approximately $2.51 billion in decentralized exchange volume and $1.31 billion in perpetual futures volume. Base recorded $930 million in DEX volume and $190 million in perpetual trading volume. The higher volumes on Solana reflect its strong position in spot trading, perpetual markets, and token launches.

Fee generation reinforces the same trend. Despite offering some of the lowest transaction costs in the industry, Solana generated approximately $584,000 in daily chain fees, compared with Base’s $73,000. The network’s scale allows even low-cost transactions to produce substantial fee revenue.

DeFi Ecosystem

Looking beyond overall capital, the composition of a DeFi ecosystem reveals how that capital is actually being used. The types of applications attracting liquidity often say more about a blockchain’s strengths than TVL alone. Although Solana and Base hold similar levels of DeFi capital, they have evolved into ecosystems with noticeably different priorities.

Trading and Liquidity

Trading is at the heart of Solana’s DeFi ecosystem. Protocols such as Jupiter and Raydium account for a large share of on-chain trading activity, while perpetual trading platforms continue to attract active market participants. Combined with low transaction costs and fast settlement, these applications have helped make Solana one of the most liquid environments for decentralized trading.

Base has also built a growing decentralized exchange ecosystem led by Aerodrome and Uniswap. However, trading activity remains well below Solana’s, reflecting the network’s greater emphasis on capital efficiency and financial services than high-frequency trading.

Lending

The picture changes when lending is considered. This is where Base stands out. Morpho has become the network’s largest DeFi protocol, alongside established platforms such as Aave. Together, they allow users to borrow against digital assets, earn yield, and deploy capital without selling their holdings, creating a deeper and more capital-efficient lending market.

Solana’s lending ecosystem continues to expand through Kamino Finance and other protocols, but lending still represents a smaller share of the network’s DeFi activity than it does on Base.

Staking and Yield

Staking tells a different story. Solana has built one of the largest liquid staking ecosystems in the industry. Jito and Sanctum allow users to stake SOL while retaining liquidity through tokenized staking positions that can be used across other DeFi applications. This has improved capital efficiency while supporting a wide range of yield-generating strategies.

Base also supports liquid staking through Ethereum-native assets, although staking plays a less central role in its DeFi ecosystem.

Ecosystem Diversity

The two networks also differ in the breadth of their ecosystems. Base hosts a larger number of DeFi protocols, benefiting from its close integration with Ethereum’s developer community. Many Ethereum applications can be deployed on Base with relatively minor modifications, resulting in a broad mix of lending markets, decentralized exchanges, infrastructure services, and consumer applications.

Solana takes a different approach. It has fewer protocols overall, but many of them generate exceptionally high levels of on-chain activity. The ecosystem has grown around a smaller set of protocols that account for a significant share of transaction volume.

Market Positioning

The metrics presented throughout this report suggest that Solana and Base are no longer competing on the same terms. Each network has carved out a distinct role within the broader blockchain ecosystem, shaped by different design choices and ecosystem priorities.

Solana: A High-Performance Financial Network

Solana has established itself as a blockchain built for speed, scalability, and low-cost execution. Those strengths have allowed it to process far more transactions and trading volume than Base, making it one of the most active networks in decentralized finance.

Its ecosystem is anchored by decentralized exchanges, perpetual trading, liquid staking, and token launches. Supported by deep stablecoin liquidity and high levels of user activity, Solana has become a natural home for applications that depend on fast execution, frequent transactions, and active markets.

Base: An Ethereum-Native DeFi Platform

The Base network has taken a different path. Rather than focusing on raw transaction throughput, it has grown as an extension of Ethereum’s financial ecosystem, prioritizing accessibility, protocol diversity, and seamless compatibility with Ethereum’s infrastructure.

Its strengths are most visible in lending, decentralized exchanges, and consumer-facing applications. Close integration with Ethereum and Coinbase gives users and developers access to familiar liquidity, infrastructure, and tools, while offering significantly lower transaction costs than Ethereum’s main network.

Together, these strengths reflect two complementary approaches to blockchain development. Solana has become the network of choice for execution-intensive markets, while Base continues to establish itself as an Ethereum-aligned platform for capital-efficient DeFi and consumer applications.

Key Risks

Both Solana and Base have established themselves as leading DeFi ecosystems, but sustaining that position will require navigating different challenges. Understanding these risks provides important context for the strengths highlighted throughout this report.

Solana

Solana’s greatest strength is also one of its key vulnerabilities. Much of its on-chain activity is driven by decentralized trading, token launches, and speculative markets, making the network more sensitive to shifts in market sentiment. During quieter market conditions, transaction volumes and fee generation can decline noticeably. Although recent upgrades have improved network stability, maintaining reliable performance as activity continues to scale remains an important priority.

Base

Base faces a different set of challenges. As an Ethereum Layer 2, its long-term growth is closely linked to the broader Ethereum ecosystem. Changes to Ethereum’s scaling roadmap, evolving user preferences, or stronger competition from Layer 2 networks such as Arbitrum, Optimism, and newer rollups could make it more difficult to attract developers, liquidity, and new applications.

Shared Challenges

Despite their different strengths, both ecosystems operate in an increasingly competitive multi-chain environment. Continued success will depend on attracting developers, retaining liquidity, and supporting sustainable application growth. Like every DeFi network, they also face broader risks, including regulatory uncertainty, smart contract vulnerabilities, and changing market conditions.

Notably, these risks do not diminish the outlook for either ecosystem. Instead, they reinforce the importance of evaluating qualitative developments alongside quantitative metrics such as TVL, network activity, and fee generation when assessing long-term ecosystem health.

Final Thoughts

The analysis shows that Solana and Base have evolved into two distinct but complementary DeFi ecosystems. Solana leads in network activity, trading volume, stablecoin liquidity, and fee generation, making it a high-performance execution layer for active on-chain markets. Base, meanwhile, has built its strengths around lending, protocol diversity, and deep integration with Ethereum, offering a capital-efficient environment for financial and consumer applications.

Rather than competing to dominate the same market, the two networks are increasingly serving different roles within the multi-chain ecosystem. Their contrasting strengths highlight how blockchain ecosystems are becoming more specialized. Evaluating long-term competitiveness, therefore, requires looking beyond TVL to include network activity, ecosystem composition, liquidity, and fee generation.

{kind=link}

{kind=link}